The Board of Directors of APS Bank plc met on 28 July 2022 and approved the attached Condensed Interim Financial Statements for the period ended 30 June 2022.

As the world is slowly transitioning into a post-pandemic era, economic instability is threatened once again from various directions – the geopolitical crisis emanating from the Russia-Ukraine war, continued global supply-side disruptions across various industries and inflationary threats which are leading to interest rate normalisation policies with cross-border economic effects. Amid these unprecedented challenges, the Bank posted record interim results which were in part reversed by the negative trends, albeit unrealised, of the investment in APS SICAV sub-funds at the Group level.

The following is an extract from the Condensed Interim Financial Statements for the period ended 30 June:

Financial Performance

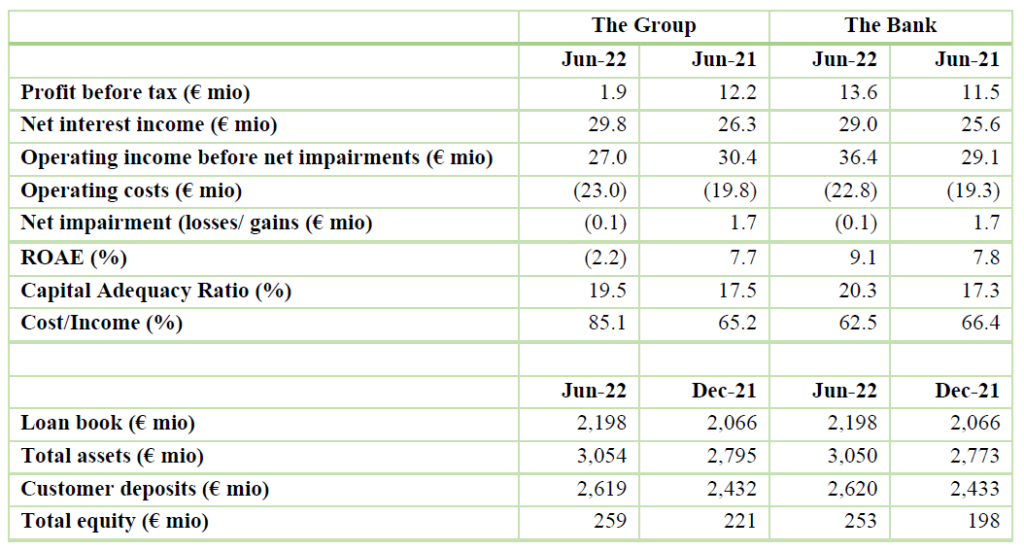

For the six months ended 30 June 2022, APS Bank registered €1.9 million profit before tax at the Group level (2021: €12.2 million) and €13.6 million profit before tax at the Bank level (2021: €11.5 million).

The Group’s revenues remain largely driven by net interest income which grew to €29.8 million for the period under review, 13.2% higher than the comparable figure of €26.3 million for 2021. Despite the tight interest rate conditions which prevailed, the growth in the lending book across both personal and commercial credit lines, and to a lesser extent in the syndicated book, created opportunities for spread. Interest payable remained around the same level of 1H2021 at €6.9 million, evincing the management’s ability to achieve more efficient cost of funding with stable interest pricing on higher deposit liabilities.

Net fee and commission income grew by 35.1% over 2021, reaching €3.8 million. This growth is driven by general business activity in loans, payments and cards and a wider customer base which provides new sources of revenue generation.

For the six months under review, the Group’s other operating income went into red territory of €6.6 million. This was largely due to the recent financial markets instability and rising fixed income yields which negatively affected the investment in the Group’s sub funds. These results reflect the performance of major bonds and equity indices, both in Malta and internationally, which have retracted by double-digit figures since the start of the year. Other operating revenues from business operations amounted to €1.6 million, increasing by €1.1 million over the comparative period.

Operating expenses for the six months ended 30 June 2022 were €23.0 million, up by €3.2 million or 15.9% on 2021. Main contributors include a higher accrual of €1.0 million in relation to the Deposit Compensation Scheme (‘DCS’) stemming from the Legal Notice 193 which brought forward a transitory period originally intended to be concluded in 2024. Staff costs also increased, reflecting rising labour prices across all levels and also the Group’s commitment to attract and retain highly skilled resources, and invest in their wellbeing and training. Other increases are noticeable for most classes of insurance, security and certain sub-contracted services. Concurrently, various initiatives are under way to improve efficiency through greater automation, digitisation of records, centralisation of processes from the network and greater use of robotics and new technologies.

Net impairment charges amounted to €0.1 million, in contrast with the €1.7 million writeback for 1H2021 that had resulted from a reversal of impairment overlays reserved in the prior, Covid-19 financial year. The Group consistently maintains a prudent view of credit in line with its risk appetite and respectful of general economic conditions and outlook.

Financial Position

Total assets stood at €3.05 billion for the reporting period, further expanding by €259.3 million or 9.3% in the past six months. This growth was largely steered by the increase in the Bank’s lending book which since end-2021 grew by 6.4% to €2.2 billion. Home lending to retail customers remained a main driver for the growth, affirming the Bank’s strong market position in this segment. The liquidity stock also grew significantly during the six months under review, with the treasury fixed-income portfolio increasing by €47.0 million to reach €375.1 million while cash and reserves with the Central Bank of Malta growing to €291.4 million compared to the €207.7 million at December 2021. Correspondingly, funding through short-term deposits increased by €205.7 million against a reduction of €18.6 million in term deposits, thus further improving the deposit portfolio mix. Amounts owed to banks stood at €70.1 million, increasing by €12.9 million on December 2021.

The period under review also saw the Bank conclude the final phase of its 2018-2022 Capital Development Plan, which has motored the growth of recent years. Early in June, the Bank closed an Initial Public Offering (IPO) of 110 million ordinary shares at an offer price of €0.62 per share, raising €66 million of new equity. The highly successful IPO, which was closed prematurely due to heavy oversubscription, led to the listing of the Bank’s entire share capital on the Malta Stock Exchange. At end-June the Bank’s CET1 ratio stands at 16.4% and the Capital Adequacy Ratio (CAR) at 20.3%.

Dividend

The Board is recommending an interim net dividend of €1,800,000 (gross dividend of €2,769,231), payable through the issuance of new ordinary shares at the nominal value of €0.25 per ordinary share. The net dividend equates to 0.50 €cents per ordinary share (gross dividend of 0.77 €cents per ordinary share). Subject to any regulatory approvals required, an Extraordinary General Meeting (“EGM”) will be convened to approve the issuance of new shares in satisfaction of this interim dividend. A separate announcement will be issued in due course announcing the date of the EGM for later in the year and after the summer period.

CEO Marcel Cassar commented:

“As anticipated in our Quarterly Financial Update of April, the first half of 2022 got off to an extraordinary start as the impetus which developed on the back of a post-Covid economic rebound experienced a new series of shocks. Most prominently, the invasion of Ukraine and the amplified supply chain issues in both energy and food prices have fuelled inflationary pressures and resultant interventions from Central Banks. Such global developments are felt also in our widely open economy through higher costs of inputs and imported goods, being partly offset by Government subsidies which however contribute to a build-up in public debt. Against this backdrop, the Maltese economy is experiencing strong growth, boosted by a healthier than expected tourism season and buoyed by the removal from the FATF grey list.

While an increase in interest rates should generally be expected to benefit bank margins, it may also impact the ability of certain borrowers to service their repayments, raising the spectre of asset quality deterioration. It is still early to forecast how this new phase of interest rate normalisation will evolve; however the Bank is entering it with a strong balance sheet, fortified by a high capital pile, ample liquidity and a conservative risk appetite resulting from a tried and tested business model.

As the market absorbs the policy adjustments and hopefully moves into a calmer environment, we should expect values of financial instruments to slowly regain the unrealised losses of recent months. Throughout this first half, APS Bank continued strengthening the fundamentals in the core business lines, asset quality and capital. Riding on the back of a hugely successful IPO, we look at the months ahead with confidence and optimism for the opportunities they may hold.”

The Condensed Interim Financial Statements for the period ending 30 June 2022 can be viewed on the Bank’s website https://www.apsbank.com.mt/financial-information