The Board of Directors of APS Bank plc met on 9 March 2023 and approved the group annual report and audited financial statements for the financial year ended 31 December 2022.

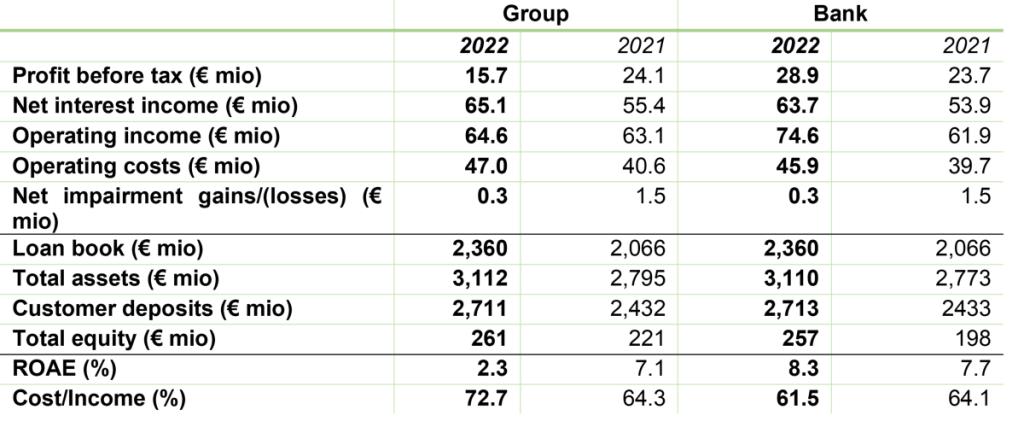

The Group posted a pre-tax profit of €15.7 million (2021: €24.1 million), while the Bank saw its pre-tax profit increase to a record of €28.9 million (2021: €23.7 million). These contrasting outcomes evince the trend already emerging in the first half of the year, as global markets were confronted by persistent economic instability and rising inflationary pressures. Notwithstanding these challenges, and despite the unrealised negative market trends at Group level, the Bank once again delivered excellent operating results.

Financial Performance

Net interest income remained a key driver of the revenue mix, growing by 17.6% from €55.4 million in 2021 to €65.1 million in 2022. An overall expansion of the Group’s home finance and commercial loan books, and in the fixed-income portfolio, were the main contributors to the growth in interest revenue, as spreads on the syndicated loan book also improved. Interest income grew by 15.5% from €69.1 million in 2021 to €79.9 million in the year under review. On the other hand, interest expense of €14.8 million increased by 7.2% on the €13.8 million of 2021, demonstrating the Group’s efficient management of its asset-liability mix and cost of funding in a period which saw interest rates move to their highest in years.

Net fee and commission income for the year of €6.9 million was marginally down on the €7.0 million of 2021. As the general growth in transactional business, card related commissions and enlarged customer base brought new sources of fee-based banking income, this was counterweighed by reductions in investment services fees, negatively impacted by the ongoing market volatility. Net gains on foreign exchange services also increased, from €0.4 million in 2021 to €1.3 million in 2022. In line with the trend of the first half of the year, albeit at a slower pace in 4Q, Group results from financial instruments ended in red territory of €10.3 million. This was mainly due to the high instability of financial markets which negatively impacted the investment in APS Funds SICAV, consolidated at Group level but not mirrored at the level of the Bank.

Operating expenses for the year grew by 15.9% to €47.0 million from €40.6 million in 2021. As expected, the main contributor was ‘employee compensation and benefits’, up by 19.4% to €26.1 million (2021: €21.8 million). The Group’s investment in human capital is intensive and continuously aiming to attract and retain the best talent, and to motivate, re-skill and up-skill staff in the face of the great attrition that is now a global phenomenon. This is reflected in all-round higher salaries, different benefits schemes (including an Employee Share Incentive Plan in 2022), investment in staff training, continuing education and well-being.

Increases were recorded across the board in other operating overheads, resulting not least from general inflation; these included regulatory and compliance costs, insurance, security and the ongoing investment in technology infrastructure, channels and digitisation, seeking the right balance between more efficiency and more sustainability (ESG/CSR) initiatives. As a result, the Group’s cost-to-income ratio deteriorated from 64.3% in 2021 to 72.7% in 2022, largely also due to the unrealised deterioration in fair value instruments. Conversely, the Bank’s cost-to-income ratio improved from 2021’s 64.1% to 61.5% in 2022.

This year too, impairments against expected credit losses resulted in a writeback of €0.3 million, reflecting the performance of customer loans and advances and the Group’s high credit underwriting standards and attitude to risk while still growing the book and actively pursuing new business opportunities.

Financial Position

As at the end of the reporting period, Group total assets stood at €3.11 billion, a year-on-year growth of 11.3% on the €2.80 billion at the end of 2021. Loans and advances to customers grew by 15.1% to €2.22 billion while the fixed income portfolio, held mainly for liquidity and income diversification purposes, grew by 40.1% to €459.6 million, as improved yield pick-up opportunities were created especially in 3Q and 4Q of the year. These quarters also saw significant activity on the syndicated loans and trade finance desks which had an overall very busy year whilst cash and reserves with the Central Bank of Malta dropped further to close the year at €85.9 million, reflecting active liquidity management and the Group’s support of Government borrowing programmes. Corresponding to the increase in the Group’s asset base, amounts owed to customers grew by 11.5% or €278.9 million, to reach €2.71 billion, despite 4Q pressures arising from competing debt issuances in the local market.

Total equity amounted to €261.5 million, compared to December 2021’s €220.8 million. As cautiously anticipated earlier in the year, market movements resulting from rising interest rates have had a direct, negative impact on reserves (through ‘other comprehensive income’). These corrections, albeit unrealised and expected to reverse fully over time, were amply compensated by the €66 million equity capital raised from the successful Initial Public Offering of June which was hugely oversubscribed within hours of opening. The Offering has had the effect of boosting the Bank’s capital adequacy ratio (CAR) and CET1 ratio to 18.8% and 15.2% respectively by the end of 3Q, a level which was maintained also at year-end.

Dividends

The Directors are recommending a final gross dividend to the ordinary shareholders of 2.68 € cents per ordinary share, totalling €9,846,153 (net dividend of 1.74 € cents per ordinary share, totalling €6,400,000). The recommendation is also to pay the dividend by way of Scrip, with each shareholder having the option to receive either cash or new ordinary shares, at an attribution price of €0.57c per new ordinary share. This final dividend is in addition to the interim dividend paid by the Bank in the fourth quarter of 2022.

The final dividend is subject to approval at the Annual General Meeting (“AGM”). Shareholders appearing on the Bank’s register of members maintained by the Central Securities Depositary of the Malta Stock Exchange as at close of trading on 14 April 2023 (trading session of 12 April 2023) will receive notice of the AGM and be entitled to receive the dividend.

Marcel Cassar, Chief Executive Officer, commented: “What seemed like a promising start to 2022 on the back of a post-pandemic economic rebound soon came to face new shocks. Prominently, the Russian invasion of Ukraine and amplified supply chain challenges in energy and food prices fuelled inflationary pressures and ensuing interventions from monetary authorities. Such international developments are felt also in our widely open economy, partly cushioned by Government subsidies which however contribute to a build-up in public debt. In this complex environment, Malta is experiencing higher economic growth, milder inflation, and lower unemployment than its EU counterparts, aided in no small way by a stronger than expected tourism recovery and buoyant retail and property markets.

Navigating through these choppy waters, we again delivered excellent results and our best Bank solo performance ever. As geopolitical tensions heightened the risk of a recession, central banks have been raising interest rates after a decade characterised by low, zero or below. 2022 saw policy makers and central bankers across borders persist in fighting inflation notwithstanding the implications for the capital markets and potentially, loan quality. In the Eurozone alone, since July the ECB increased its deposit rate progressively to 2.50% from -0.5%, making it the largest and fastest increase in rates in the monetary union’s history. As banks adapt their strategies to the reality of higher interest rates, we shall manage this new scenario with the concerns of all our customers in mind.

Despite the fair value impacts on our investment portfolios, we remain comfortable that these are of sound credit quality and that the slide in valuations will continue to be clawed back over the coming financial periods. 2023 has started on solid footing and we look forward to more exciting prospects for the APS Group, encouraged by strong customer confidence in our model and as opportunities to gain further market share continue to unfold.”

The Annual Report and Audited Financial Statements for the year ended 31 December 2022 can be viewed on the Bank’s website: https://www.apsbank.com.mt/financial-information